The Audit Report Sample & Engagement Letter You Need to See: A Comprehensive Guide

Navigating the world of audits can feel overwhelming, especially when you’re dealing with complex financial documents. Two of the most crucial pieces of this puzzle are the audit report itself and the engagement letter. This guide provides a clear overview of these documents, offering insights into what they entail, their importance, and how they work together. We’ll also provide a look at a sample audit report and engagement letter, equipping you with the knowledge you need to understand and interpret these critical financial tools.

Understanding the Audit Report: Your Window into Financial Health

The audit report is the culmination of an independent auditor’s examination of a company’s financial statements. It’s a formal document that provides an opinion on whether those statements fairly present the company’s financial position, results of operations, and cash flows, in accordance with Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS). Think of it as a report card for your company’s finances, issued by an unbiased third party.

Here’s what you’ll typically find within an audit report:

- Title: Clearly indicates the report’s purpose (e.g., “Independent Auditor’s Report”).

- Addressee: Identifies the entity for whom the report is prepared (e.g., shareholders, board of directors).

- Introductory Paragraph: States that the auditor has audited the financial statements and lists the specific statements examined (e.g., balance sheet, income statement, statement of cash flows).

- Management’s Responsibility: Outlines management’s responsibility for preparing the financial statements and maintaining internal control over financial reporting.

- Auditor’s Responsibility: Details the auditor’s responsibility to express an opinion on the financial statements based on the audit. This section usually includes a description of the audit process.

- Opinion: This is the heart of the report. The auditor expresses an opinion on whether the financial statements are presented fairly, in all material respects, in accordance with the applicable financial reporting framework. There are four main types of audit opinions:

- Unqualified/Clean Opinion: The financial statements are presented fairly.

- Qualified Opinion: The financial statements are presented fairly, except for a specific matter.

- Adverse Opinion: The financial statements are not presented fairly.

- Disclaimer of Opinion: The auditor is unable to express an opinion due to limitations in the scope of the audit.

- Basis for Opinion: Explains the basis for the auditor’s opinion, including the procedures performed and any significant findings.

- Signature and Date: Includes the auditor’s signature, the name of the audit firm, and the date the report was issued.

- Auditor’s Address: Provides the auditor’s contact information.

Sample Audit Report Snippet (Illustrative):

“Independent Auditor’s Report

To the Shareholders of ABC Company,

We have audited the accompanying financial statements of ABC Company, which comprise the balance sheet as of December 31, 2023, and the related statements of income, changes in equity, and cash flows for the year then ended, and the related notes to the financial statements.

In our opinion, the financial statements present fairly, in all material respects, the financial position of ABC Company as of December 31, 2023, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in [Country].”

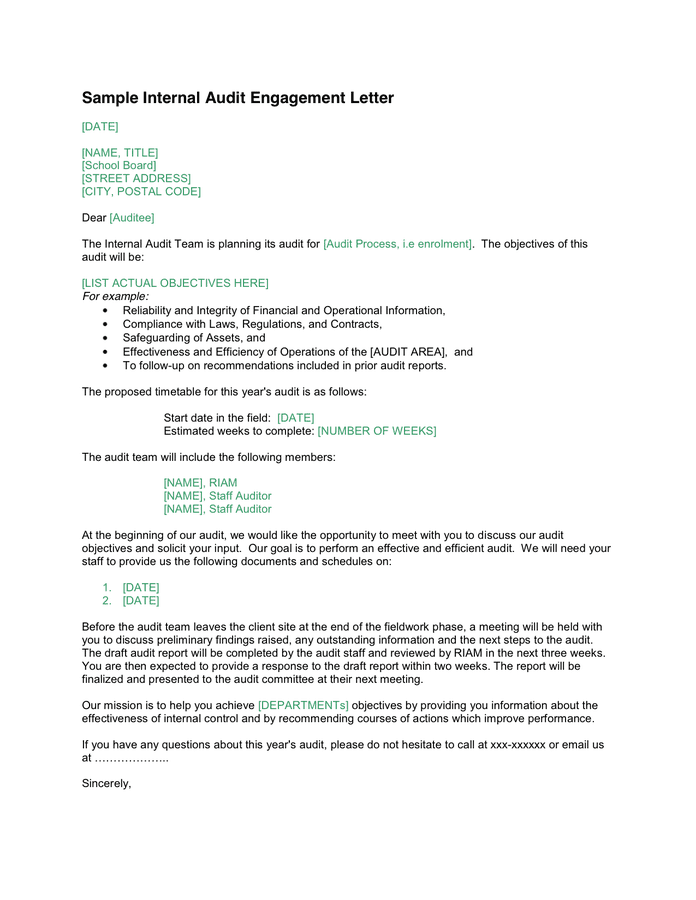

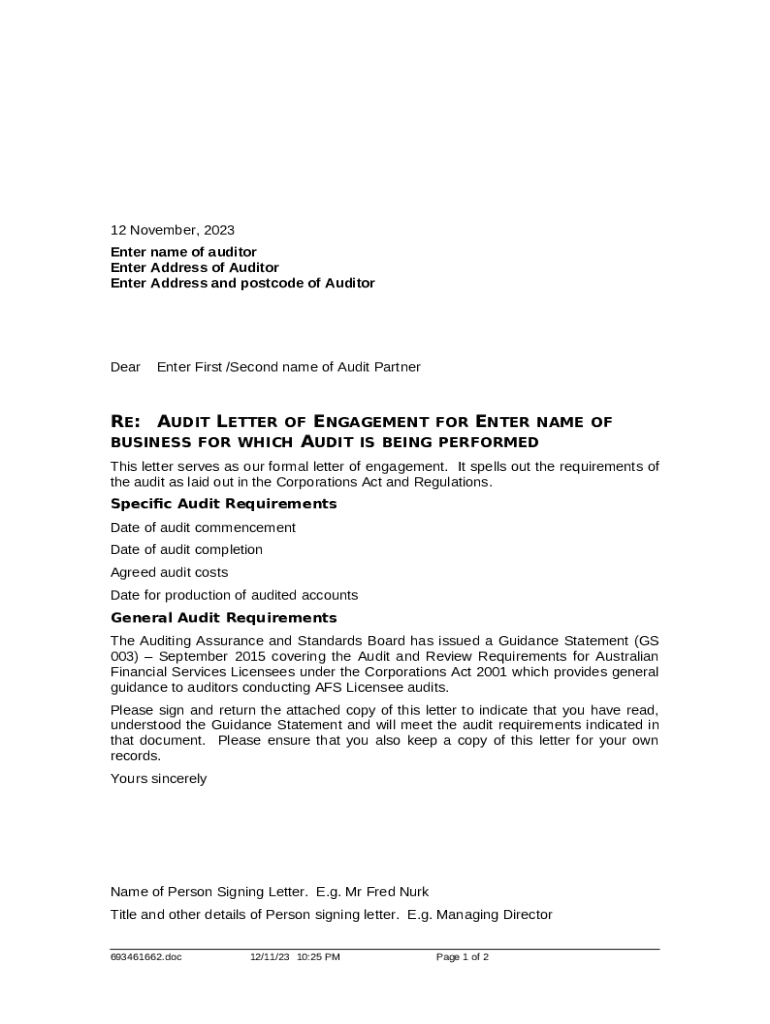

Deciphering the Engagement Letter: The Blueprint for the Audit

The engagement letter is a crucial agreement between the auditor and the client. It outlines the scope of the audit, the responsibilities of both parties, the fees, and the expected timeline. It serves as a contract, clarifying the terms of the audit engagement and minimizing misunderstandings. Think of it as a detailed plan for the audit process.

Key components typically found in an engagement letter:

- Identification of the Client and the Audit Period: Clearly states the name of the company being audited and the financial period covered by the audit.

- Scope of the Audit: Defines the specific financial statements and areas that will be examined. This could include, but is not limited to, revenue recognition, inventory valuation, and accounts payable.

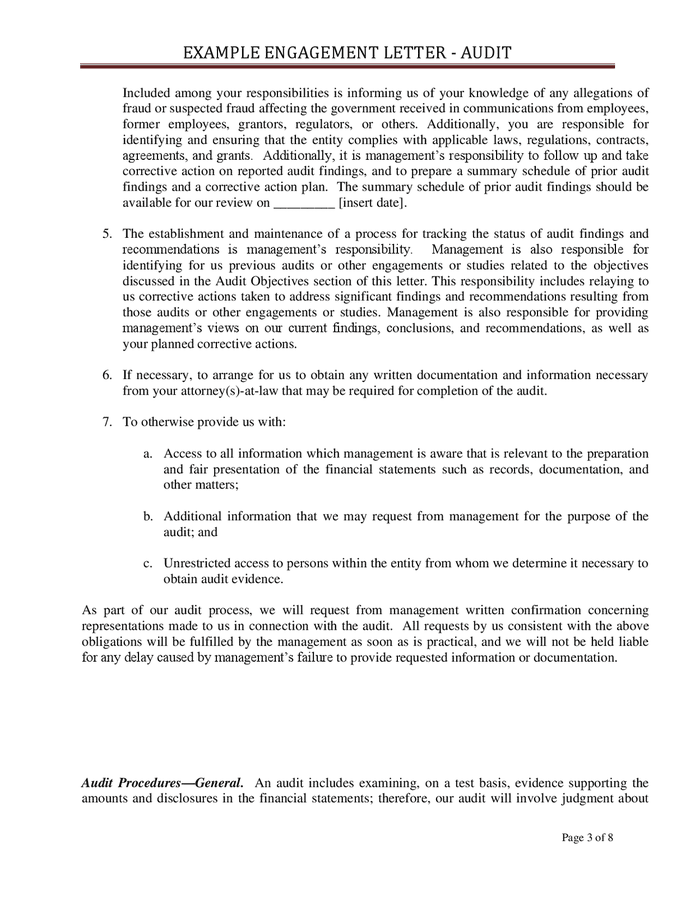

- Responsibilities of Management: Outlines management’s responsibilities, such as preparing the financial statements, providing access to all relevant information, and maintaining effective internal controls.

- Responsibilities of the Auditor: Describes the auditor’s responsibilities, including conducting the audit in accordance with relevant auditing standards and expressing an opinion on the financial statements.

- Audit Fees and Payment Terms: Specifies the fees for the audit and the payment schedule.

- Reporting: Details how the auditor will communicate the audit findings, including the format and content of the audit report.

- Timing and Deadlines: Outlines the expected timeline for the audit, including key dates for fieldwork, report issuance, and meetings.

- Use of the Report: States the intended use of the audit report, typically for distribution to shareholders, regulators, or other stakeholders.

- Legal Matters: Addresses any legal aspects of the engagement, such as confidentiality and liability.

- Signatures: Requires signatures from both the auditor and a representative of the client, indicating agreement to the terms of the engagement.

Sample Engagement Letter Snippet (Illustrative):

“Engagement Letter

[Date]

[Client Name]

[Client Address]

Dear [Client Contact Person],

This letter confirms our understanding of the terms and objectives of our audit of the financial statements of [Client Name] for the year ended December 31, 2023.

Scope of the Audit: We will conduct an audit of the financial statements of [Client Name], which comprise the balance sheet, the statement of income, the statement of cash flows, and the statement of changes in equity for the year ended December 31, 2023, in accordance with auditing standards generally accepted in [Country].

Responsibilities of Management: Management is responsible for the preparation and fair presentation of the financial statements in accordance with [Accounting Framework], for the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error, and for providing us with access to all information of which management is aware that is relevant to the preparation and fair presentation of the financial statements, such as records, documentation, and other matters.

Audit Fees: Our fees for this engagement will be [amount], payable as follows: [payment schedule].

Please sign and return the enclosed copy of this letter to indicate your agreement with the terms outlined above.

Sincerely,

[Auditor Name]

[Audit Firm Name]”

How the Audit Report and Engagement Letter Work Together

The engagement letter lays the groundwork for the audit, while the audit report is the ultimate product. The auditor performs their work, as defined in the engagement letter, and then issues the audit report based on their findings. The engagement letter provides the legal framework for the audit, and the audit report provides the conclusion of the process. They are inextricably linked and vital for a successful and transparent audit.

Conclusion: Empowering Informed Financial Decisions

Understanding the audit report and engagement letter is critical for anyone involved in financial reporting, from business owners and executives to investors and creditors. By familiarizing yourself with these documents, you gain valuable insights into your company’s financial health and the integrity of its reporting. This knowledge empowers you to make informed decisions and confidently navigate the complexities of the financial landscape.

FAQs

1. What is the difference between an unqualified and a qualified audit opinion?

An unqualified opinion (also known as a clean opinion) means the auditor believes the financial statements are presented fairly, in all material respects, according to the applicable accounting standards. A qualified opinion means the auditor believes the financial statements are presented fairly, except for a specific matter or limitation in scope.

2. What are the implications of an adverse audit opinion?

An adverse opinion is the most negative type of opinion. It indicates that the auditor believes the financial statements are not presented fairly and contain material misstatements. This often raises serious concerns about the company’s financial health and the reliability of its financial reporting.

3. How long does an audit typically take?

The duration of an audit can vary significantly depending on the size and complexity of the company, the scope of the audit, and the quality of the company’s internal controls. A small business audit might take a few weeks, while a large, multinational corporation could take several months. The engagement letter will specify the expected timeline.

4. Why is the engagement letter important?

The engagement letter is important because it clearly defines the scope of the audit, the responsibilities of both the auditor and the client, and the terms of the engagement. This helps to prevent misunderstandings and ensures a smooth and efficient audit process.

5. Can I negotiate the terms in the engagement letter?

Yes, it is possible to negotiate certain terms in the engagement letter, particularly regarding fees, deadlines, and the scope of the audit. However, the core responsibilities of both parties and the fundamental auditing standards cannot be altered.